FAQ

The CCAF periodically publishes a list of authorised management companies and credit institutions on its website, along with the activities for which they are authorised.

Foreign financial products may be marketed by firms and credit institutions authorised in Monaco, under their own liability.

However, with some exceptions¹, firms that are not authorised by the CCAF are not permitted to market financial services, instruments, or products to private residents of Monaco, whether such marketing is solicited or not. Unsolicited distance marketing is also prohibited, except where the person domiciled in the Principality is a client of the firm that is not authorised by the CCAF.

Once it receives a complete application, the CCAF has up to six months in which to make a decision on whether to grant authorisation. In practice, if the application is straightforward, a decision could be made sooner.

No, authorisation from the CCAF is entirely free of charge.

The minimum share capital is set by Article 1 of Sovereign Ordinance No. 1,284, amended. It depends on the financial activity carried out:

- For third-party portfolio management: 450,000 euros, except in certain special cases²

- For Monegasque fund management: 150,000 euros for up to 250 million euros of assets under management, plus 40,000 euros of extra capital per additional tranche of 200 million euros

A company that manages funds whose shares are offered exclusively in the Principality may have share capital equal to not less than 150,000 euros or 0.5% of the assets under management, up to a limit of 750,000 euros. However, the minimum may be reduced to 150,000 euros where 50% of the capital is held by a credit institution or insurance or reinsurance company, provided that the institution in question has share capital of at least 2 million euros (Article 32 of Sovereign Ordinance No. 1,285). - For reception-transmission of orders on behalf of third parties: 300,000 euros, except in certain special cases²

- Advisory services for third-party portfolio management, the management of Monaco-registered funds, and reception-transmission of orders on behalf of third parties: 300,000 euros, except in certain special cases²

- For management of foreign-registered collective investment vehicles: 450,000 euros, except in certain special cases²

If the firm carries out more than one financial activity, the highest minimum share capital requirement applies.

No. If an authorised firm carries out both of these activities for the same client, it must require segregated accounts to be opened with the custodian institution.

The controls to be carried out by regulated entities are laid down by Article 23 of Act No. 1,338, amended, which states that “authorised firms are required to observe the prudential rules and rules of conduct stipulated by Sovereign Ordinance.” Article 6 of Sovereign Ordinance No. 1,284, amended, requires authorised firms to have “an administrative organisation” and “adequate security and internal and external control mechanisms.”

When applying for authorisation, the firm must provide the CCAF with a description of its control mechanisms and procedures, along with the CVs of the individual officer responsible for control of management activities. This primarily concerns the officers responsible for level 2 internal controls (see below). Depending on the firm, this role may be referred as “internal control officer” or “compliance officer”. Where, in view of its size and activities, a firm has both an internal control officer and a compliance officer, the latter’s CV may be requested by the CCAF. More generally, the CCAF may ask for any other information or documentation it deems necessary.

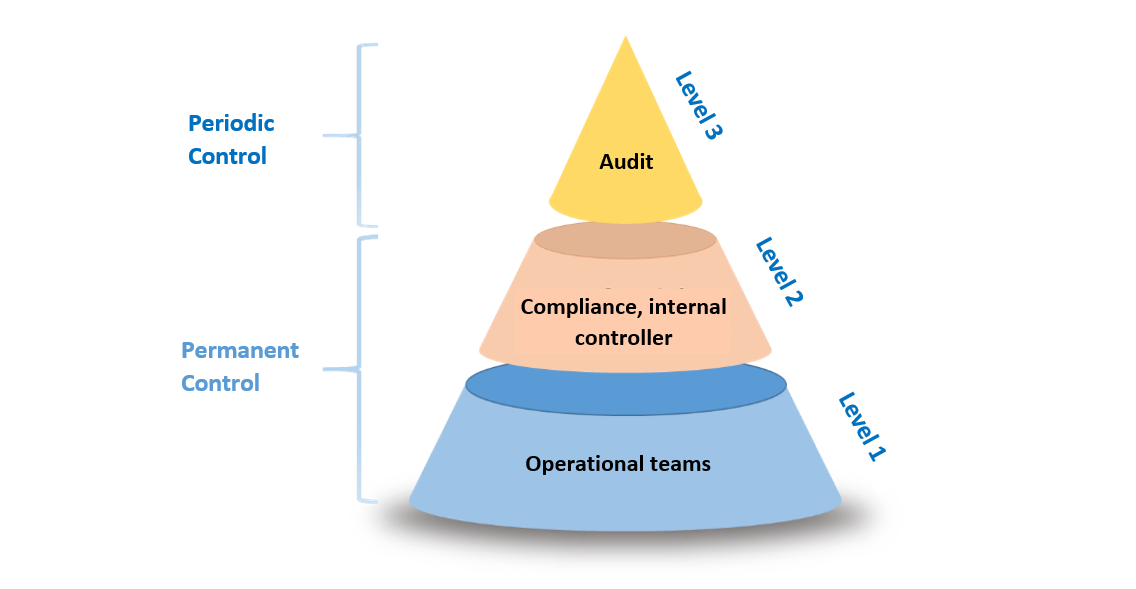

In accordance with the above provisions, authorised firms are required to establish and maintain a compliance and internal control system that includes three levels of controls:

- Level 1 controls: these controls are carried out by operational personnel. Their purpose is to ensure that the firm’s policies and procedures are properly followed.

- Level 2 controls: these controls are intended to ensure that level 1 controls have been correctly applied.

In principle, individuals who actively participate in compliance checks must play no part in providing the services or carrying out the activities that they are called upon to control. It is also recommended that the internal control/compliance officer should report directly to one of the firm’s strategic orientation and management officers (referred to as the “ROSG”).

Where anomalies are found or the control system needs to be reviewed (this may entail a review of procedures, changes to the control system, etc.), level 2 controls should draw the ROSG’s attention to the issues identified and the remedial measures that need to be taken. - Level 3 controls: these form the periodic control system. The main purpose is to assess the authorised firm’s internal control system to ensure that it is suitable and effective. These controls are generally carried out on a multiannual basis.

When examining an application for authorisation, the CCAF will look at the organisational choices made by the firm in the area of internal control, and the effectiveness of the control functions put in place. This is done on a case-by-case basis. Some of the points mentioned above may be relaxed depending on the size of the firm, the nature, scale, and complexity of its activities, and whether or not it is part of a group. The same applies to the possibility of outsourcing some controls, although it is important to remember that where controls are outsourced, the firm retains full responsibility for ensuring it complies with statutory provisions.

In all cases, it is the firm’s duty to review its internal control system regularly, taking into account any changes to its activities, and any anomalies or difficulties identified in the area of internal control.

Authorised firms must take all reasonable steps to prevent conflicts of interest. They must establish and adopt written rules governing the management of conflicts of interest, appropriate for the size, organisation, and nature of the firm, and the scale and complexity of its activities. They must also keep a register of conflicts of interest and update it regularly.

Yes, a firm of credit institution that is authorised under the terms of Act No. 1,338 may delegate one or more of its activities, provided it satisfies certain conditions.

In particular, the firm is not permitted to delegate the entirety of its activities, and it retains fully liable for any activities outsourced. It must monitor the delegated activity at all times.

The task of managing Monegasque funds may only be delegated to a foreign company if the CCAF has a cooperation agreement with the regulator in the country concerned (except in certain special circumstances³).

Finally, if there is a management mandate in place, part of the third-party portfolio management activities may be delegated, but only if the client has given their express prior consent to the delegation arrangements and object.

Banking, financial, and ESG certification has two components: technical and ethical. It is only mandatory for certain categories of personnel (and their line manager): managers, sales operatives, financial analysts and traders.

For the technical component, where individuals are able to produce similar qualifications issued by foreign authorities, these may be recognised and accepted as equivalents by the Professional Certifications Committee. The request for exemption should be sent to the President of the Professional Certifications Committee (AMAF – 7 rue du Gabian – MC 98000 Monaco), accompanied by the individual’s CV and a copy of the equivalent qualification.

However, no exemption may be granted neither for the ethical component, which concerns regulatory requirements specific to Monaco, nor the ESG section.

A grandfather clause does apply for staff who were already in post before 2 May 2014 or hold the professional certification created by Ministerial Decree No. 2014-168.

No.

Financial activities internal control certification is mandatory only for the internal control officer and their staff.

No exemptions are possible.

However, a grandfather clause does apply for staff who have been in post in Monaco continuously for over five years on the date of entry into force of Sovereign Ordinance N°9.737 (11 February 2023).

No, the CCAF only supervises the financial activities of credit institutions. Their banking transactions are supervised by the French ACPR.

No, it is not permitted to withhold information from the CCAF on grounds of professional secrecy, except by notaries and other representatives of the law. Auditors are not bound by professional secrecy in respect of the Commission specifically for the application of Act No. 1,338, amended.

They could potentially incur administrative and/or criminal penalties.

Administrative penalties may be imposed by the CCAF, following adversarial proceedings in which all parties are entitled to a fair hearing, as described in Articles 36 et seq. of Act No. 1,338, amended.

If an authorised firm or credit institution breaches its obligations under Act No. 1,338, amended, and its implementing regulations, the Commission may issue a formal warning or a reprimand. In certain cases, listed in Article 34 of the Act, the Commission may suspend authorisation temporarily (for up to six months) or withdraw it permanently.

1 – Except where the person domiciled in the Principality is an institutional investor, an authorised firm or a client of an authorised firm where the marketing activity is carried out through it.

2 – This figure may be reduced to 150,000 euros where 50% of the capital is held by a credit institution or insurance or reinsurance company, provided that the institution in question has share capital of at least 2 million euros.

3 – Where fund units are offered only in the Principality.